The Impact of Intranational Trade Barriers

on Exports: Evidence from a Nationwide

VAT Rebate Reform in China

Jie Bai and Jiahua Liu

CID Faculty Working Paper No. 373

December 2019

© Copyright 2019 Bai, Jie; Liu, Jiahua; and the President

and Fellows of Harvard College

at Harvard University

Center for International Development

Working Papers

The Impact of Intranational Trade Barriers on Exports:

Evidence from a Nationwide VAT Rebate Reform in China

Jie Bai Jiahua Liu

∗

December 13, 2019

Abstract

It is well known that various forms of non-tariff trade barriers exist within a country.

Empirically, it is difficult to measure these barriers as they can take many forms. We take

advantage of a nationwide VAT rebate policy reform in China as a natural experiment to

identify the existence of these intranational barriers due to local protectionism and study

the impact on exports and exporting firms. As a result of shifting tax rebate burden, the re-

form leads to a greater incentive of the provincial governments to block the domestic flow of

non-local goods to local export intermediaries. We develop an open-economy heterogenous

firm model that incorporates multiple domestic regions and multiple exporting technologies,

including the intermediary sector. Consistent with the model’s predictions, we find that ris-

ing local protectionism leads to a reduction in interprovincial trade, more “inward-looking”

sourcing behavior of local intermediaries, and a reduction in manufacturing exports. Anal-

ysis using micro firm-level data further shows that private companies with greater baseline

reliance on export intermediaries are more adversely affected.

∗

Contact information: Bai: Harvard Kennedy School, e-mail: jie [email protected]ard.edu; Liu: Harvard Kennedy School,

email: jiahua [email protected]ard.edu. We thank Nikhil Agarwal, Pol Antras, Abhijit Banerjee, Panle Jia Barwick, Arnaud

Costinot, Dave Donaldson, Jack Feng, James Harrigan, Marc Melitz, Benjamin Olken, Gerard Padro, Robert Townsend,

Jeffery Wang, and lunch, seminar and conference participants at ASSA annual meeting, Cornell, Harvard, MIT, and

NEUDC for helpful discussions and comments. All errors are our own.

1

1 Introduction

“Aside from tariff barriers (i.e., special charges levied at roadblocks), non-tariff methods such as

physical barriers, outright prohibition, low-interest loans, and other financial benefits for commercial

establishments marketing local goods, fines for commercial establishments marketing nonlocal goods,

legal restrictions on price differences between local and nonlocal goods sold in commercial establishments,

local purchasing quotas, and administrative trivia (e.g

˙

, medical, sanitation, epidemic prevention, product

quality, measurement, and other such licenses and certificates) were used to hamper trade in products

in a market economy.” (Young, 2000)

It is

well known that various forms of non-tariff barriers exist within a country. While local governments

cannot block their borders or impose tariffs, their influence over the local regulatory apparatus can allow

them to impose significant non-tariff barriers to discourage non-local firms and non-local goods from

entering the local markets. Young (2000) gives many examples of such non-tariff barriers in the Chinese

context. These barriers are especially likely to arise in countries’ where political and fiscal powers are

decentralized to subnational units. However, despite the general consensus on the existence of these local

trade barriers, we know relatively little about how costly they are in terms of real economic outcomes:

widespread interprovincial trade wars are very different from occasional protectionist practices. What

makes this a challenging empirical problem to study is precisely the fact that these local barriers can

take many forms, and unlike tariff barriers, they are difficult to measure or even just to observe.

In this study, we take advantage of a nationwide VAT rebate policy reform in China in 2004 as a nat-

ural experiment to first identify the existence of intranational trade barriers due to local protectionism

and then to quantify the impact on exports and firm performance. As a result of the shifting tax rebate

burden, the reform leads to a greater incentive of the provincial governments to block the domestic flow

of non-local goods to local export intermediaries. By exploring a unique feature of the transaction-level

Chinese Customs Data that allows us to trace the sourcing locations of the export intermediaries, we

show that the intermediaries indeed become more “inward-looking” after the reform.

To go beyond the descriptive evidence and examine the impact on interprovincial trade and man-

ufacturing exports, we develop a theoretical model to guide the empirical analysis. The model is built

on the standard open-economy heterogeneous firm model by incorporating multiple domestic regions

and multiple exporting technologies, including the intermediary sector. We model the intermediary

technology following Ahn, Khandelwal, and Wei (2011), but with a new focus on the intermediary’s

2

role of domestic sourcing. The model predicts a fall in interprovincial trade (related to exporting via

intermediaries) and a reduction in manufacturing exports as a result of rising local protectionism.

To bring the theory to the data, we explore subnational variations in rebate burden and exposure

to the reform. First, for each province, we construct a measure of predicted rebate burden based on the

local intermediaries’ sourcing patterns prior to the reform and the tax rebate formula. Consistent with

the descriptive evidence, we find that intermediaries located in provinces with a higher predicted rebate

burden become more “inward-looking” after the reform. Specifically, they source from fewer non-local

provinces and source a greater fraction of local goods. The results are robust to controlling for province

and time fixed effects, time-varying rebate rates, and province-specific time trends.

Using a difference-in-difference framework, we then examine the impact of increasing provincial

rebate burden on interprovincial trade flows of indirect exports (i.e., exports via intermediaries). Our

estimate implies a trade elasticity of 1.2 with respect to provincial rebate burden. The magnitude is

comparable to existing estimates in the trade literature with respect to physical transportation costs,

indicating that political barriers can act as important frictions in hindering domestic trade.

Next, we examine the impact on manufacturing exports and manufacturing firms. To do so, we

construct a measure of reform exposure for each province-industry as the weighted average of the

predicted rebate burdens, where the weights are given by a province-industry’s baseline reliance on

intermediaries located in different provinces. The results show that greater exposure to the reform

leads to reductions in both indirect exports as well as total exports. Using the NBS annual survey of

manufacturing firms, we show that, while some firms manage to switch to direct exporting, most of the

negative impact falls on private firms with a greater reliance on export intermediaries at baseline.

Last but not least, we explore the firm-level Customs data to shed light on local government behavior.

While systematic documentation of the protectionist practices does not exist, we find suggestive evidence

that local governments may target large intermediaries, either due to limited administrative capacity or

fixed costs of the intervention technology. However, beyond that, local officials do not appear to employ

additional local information in the targeting, such as an intermediary’s history of non-local purchase

and its product mix.

The study relates to the literature on domestic trade frictions. Ramondo, Rodr´ıguez-Clare, and

Sabor´ıo-Rodr´ıguez (2016) find that domestic frictions are key to explaining the discrepancy between

standard trade models and the data. Costinot and Donaldson (2016) find substantial gains from eco-

nomic integration among US agricultural markets from 1880-2002. More recent studies have quantified

domestic trade costs due to geographical barriers and poor transportation infrastructure (for example,

3

Limo and Venables (2001), Donaldson (2010), Banerjee, Duflo, and Qian (2012), and Faber (2014),

Anderson, Milot, and Yotov (2014), Atkin and Donaldson (2015), and Co¸sar and Fajgelbaum (2016)).

However, as discussed above, domestic trade barriers can take other forms. Lacking a good transporta-

tion network is responsible for the lack of greater economic integration, but it may not explain the full

story. Our findings show that political barriers imposed by local governments play an important role.

The paper also contributes to the literature on local protectionism (for example, Young (2000),

Naughton (2003), Bai, Du, Tao, and Tong (2004), Poncet (2003), Poncet (2005), and Holz (2009)).

There are two strands of this literature: the first hinges on patterns of regional convergence as evidence

of rising protectionism (Young, 2000). However, a challenge with this approach is the lack of a theoretical

yardstick with which to evaluate the changes: reversal of inefficient patterns of specialization can be

efficiency enhancing. The second strand of the literature relies on provincial input-output tables to

estimate the border effect from a gravity equation (Poncet, 2005). The estimate may be confounded by

the presence of non-traded local goods and non-homothetic preferences.

1

We use micro firm-level data

to address some of the limitations and identify local trade barriers under relatively weak assumptions.

Our study is closely related and complementary to a concurrent paper by Barwick, Cao, and Li (2017),

in which the authors document local protectionism from “home bias” in passenger vehicle purchasing.

We focus on the supply side and study firms’ responses in light of rising local protectionism.

Finally, the study relates to the literature on resource misallocation. Institutions that distort the

efficient allocation of resources can have a sizable effect on economic outcomes. Hsieh and Klenow

(2009) estimate that the distortions in the Chinese economy reduce manufacturing productivity by 30%

to 50%. Brandt, Tombe, and Zhu (2013) estimate a large distortion on aggregate TFP due to inefficient

factor inputs allocation within and between provinces in China. There has been a growing body of work

that tries to uncover particular sources of misallocation, including industrial policies and labor market

frictions (for example, Khandelwal, Schott, and Wei (2013), Fajgelbaum, Morales, Serrato, and Zidar

(2018) and Garicano, Lelarge, and Van Reenen (2016)). We show that local protectionism induced by

national tax policies can act as a potential source of resource misallocation.

The remainder of the paper is organized as follows. Section 2 describes the policy background.

Section 3 presents the model. Section 4 describes the data. Section 5 discusses the empirical strategy.

Section 6 presents the empirical results. Section 7 concludes.

1

Most of the studies rely on aggregate data. However, one limitation of the Chinese IO table is that it only reports a

net trade value, which aggregates the total net trade with the rest of China and the rest of the world. As a result, the

gravity equation estimates are also sensitive to functional form assumptions, including measures of distance between a

given province and the rest of China.

4

2 Background

2.1 Export Value-Added Tax Rebate Policy and the 2004 Reform

Value-added tax (VAT) is a general broad-based tax assessed on incremental value at each stage of the

production of goods and services. In China, the VAT rate is 17%, and it applies to most goods and

services that are bought or sold for use. The export tax rebate policy is such that the VAT paid for

exported goods can be refunded in whole or in part.

2

The idea is to remove taxes paid in all stages of

the production process so that the goods can enter the international markets without tax.

3

Under the

regime, when a manufacturer exports through an export intermediary (i.e., a foreign trade company,

or FTC), the FTC is entitled to a “Pay-First-and-Refund-Later” VAT refund treatment (Chan, 2008):

initially the FTC pays an output-tax-inclusive price to the manufacturer; after completing the export

5

transaction, the FTC can collect a partial or full refund of the tax paid earlier.

4

Prior to 2004, the central government was solely responsible for financing the VAT rebates —

after completing an export transaction, an exporter first receives its VAT refund from the provincial

government, which then receives the same amount of payment from the central government at the end

of each fiscal year. However, the rapid growth of exports after China entered the WTO in 2001 led

to a large backlog of rebate payments and put severe fiscal pressure on the central government. In

response to the mounting financial burden, the central government implemented a major reform in 2004

2

The WTO Agreement on Subsidies and Countervailing Measures (SCM, Article 1.1a) allows members to provide

rebates on export duties as long as the rebate does not exceed the full extent of the duty imposed. Thus, in contrast to

other trade policies such as export subsidies, VAT rebates are sanctioned by the WTO.

3

In practice, the VAT rebates have remained incomplete for most commodities in China, and the rebate rates have been

adjusted over time as a policy tool to boost exports (Bai, Wang, and Zhong, 2011).

4

In general, the exact VAT rebate formula varies across different business types. There are three VAT refund treatments

applied to different types of exporters:

1. Pay-first-and-refund-later: an exporter, typically a commercial enterprise, can have the VAT incurred during the

production process refunded in whole or in part prior to export. The refund rate could be lower than the VAT rate

charged. No tax burden is incurred if the refund rate equals to the VAT rate. This paper mainly analyzes the result

of a change to this treatment.

2. Exempt-credit-refund: an exporter, typically a production enterprise, will get refunded for the excess if the amount

of input VAT, from which the disallowed credit has already been deducted, is bigger than the VAT payable for the

current period. Exempt refers to the exemption of VAT for exports, and credit refers to the input VAT paid for the

purchase used in the manufacture of exports that will be offset against the output VAT paid on local sales.

3. Tax exempt: an exporter, typically an export-processing enterprise, is not entitled to a VAT refund because either it

has not previously paid any input VAT on exports or it has paid input VAT but the refund policy is not applicable.

An example is bonded materials directly imported for use in export processing.

5

In general, a Chinese manufacturer can export through an FTC in two ways: either by simply selling the goods to the

FTC or by authorizing the FTC as an exporting agent (Wang, 2019). Before 2007, most manufacturer-FTC partnership

was in the form of the former, in which the “Pay-First-and-Refund-Later” treatment applies.

5

that shifted part of the rebate burden to the provincial governments.

6

In particular, the new policy

stipulates that, for the amount of rebates claimed by an exporter, the central government would finance

75% of the rebates, with the remaining 25% covered by the provincial government, depending on where

the exporter is located.

7

The justification for the 75/25 sharing rule is that the VAT revenue is shared

between the central and provincial governments according to this ratio.

2.2 Rising Local Protectionism

While the reform alleviated the fiscal pressure on the central government, it created an unintended

consequence — it led to a strong incentive for provincial governments to discourage local FTCs from

servicing non-local manufacturers. Operating as export intermediaries, FTCs do not engage in man-

ufacturing activities but instead specialize in export services. They procure goods produced by other

manufacturing firms and resell them to the international markets after simple processing, such as re-

packaging and re-labeling. An FTC can source goods from manufacturers located in its own province or

from manufacturers located in other provinces. Under the post-reform rebate regime, for any non-local

goods sourced and exported by an FTC, the provincial government of the FTC has to finance 25% of

the VAT rebates despite the fact that it has not collected the VAT revenue share in the first place,

which is paid to the provincial government where the manufacturer is located.

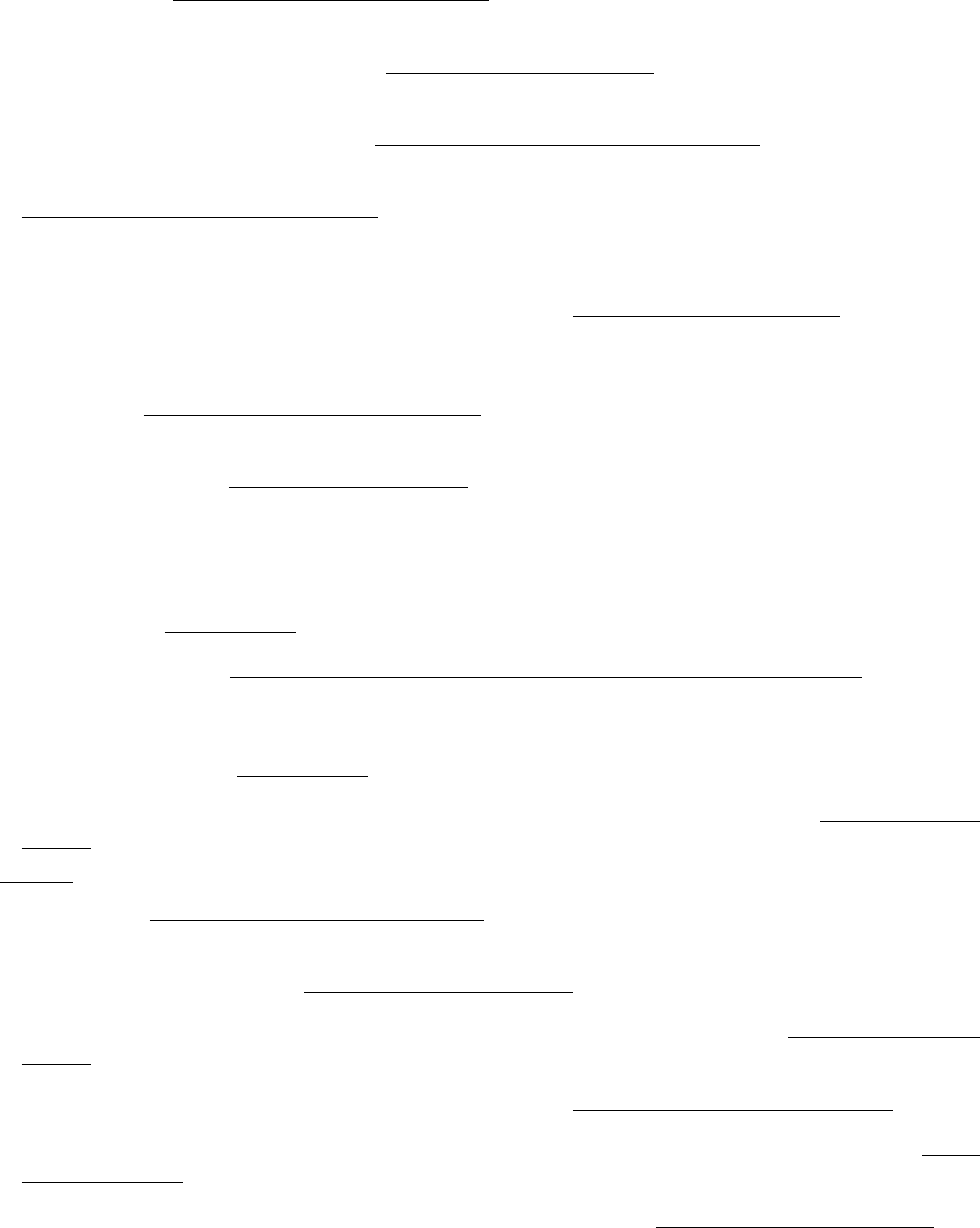

Figure 1 provides a graphical illustration. In this example, an upstream manufacturing firm produces

t-shirts worth 1000 USD. At the point of transaction between the manufacturer and the FTC, the latter

pays the former 1000 USD plus 17% VAT. The VAT revenue is split between the upstream province

and the central government. At the end of the transaction, the manufacturing firm issues a VAT invoice

to the FTC, with which the latter can get the tax refunded after exporting the t-shirts. Prior to the

reform, the entire rebates were financed by the central government, but after the reform, the downstream

province where the FTC is located has to finance 25% of the rebates, even though it has not collected the

revenue share. This generates a large fiscal burden on the provinces where many FTCs are located. As

a result, the local governments have a strong incentive to block non-local goods, either by discouraging

the activities of the intermediary sector in general or by asking its local FTCs to divert more sourcing

toward local goods.

6

Note that the same reform also adjusted the rebate rates for many commodities across five distinct levels: 5%, 8%,

11%, 13%, and 17%, depending on the product category. In our empirical analysis, we collect detailed data on VAT rebate

rates and control for the concurrent changes across product sectors.

7

The sharing rule was later adjusted to 92.5/7.5 in 2005, in part due to the concerns over rising local protectionism

— see Section 2.2. Since 2015, it has completely reverted back to the original scheme, in which the central government

finances 100% of the rebates.

6

Media reports abound that the reform led to rising local protectionism in the ensuing years. Un-

fortunately, there has not been any systematic documentation of the protectionist measures introduced

by the local governments due to the illegal nature of such activities.

8

To understand the situation, we

conducted extensive research into media and government reports and interviewed a number of people

working in the intermediary sector. One specific protectionist measure stands out from these qualitative

accounts, which is through deliberate delays of VAT rebates for non-local goods: in particular, when

the local tax bureau receives a lot of VAT invoices for non-local goods filed by an FTC, it could delay

the refund to the firm. There were many reports of such delays in VAT rebates in the early 2000s (for

example, Zhong (2004); Wen (2005); Wu (2004)).

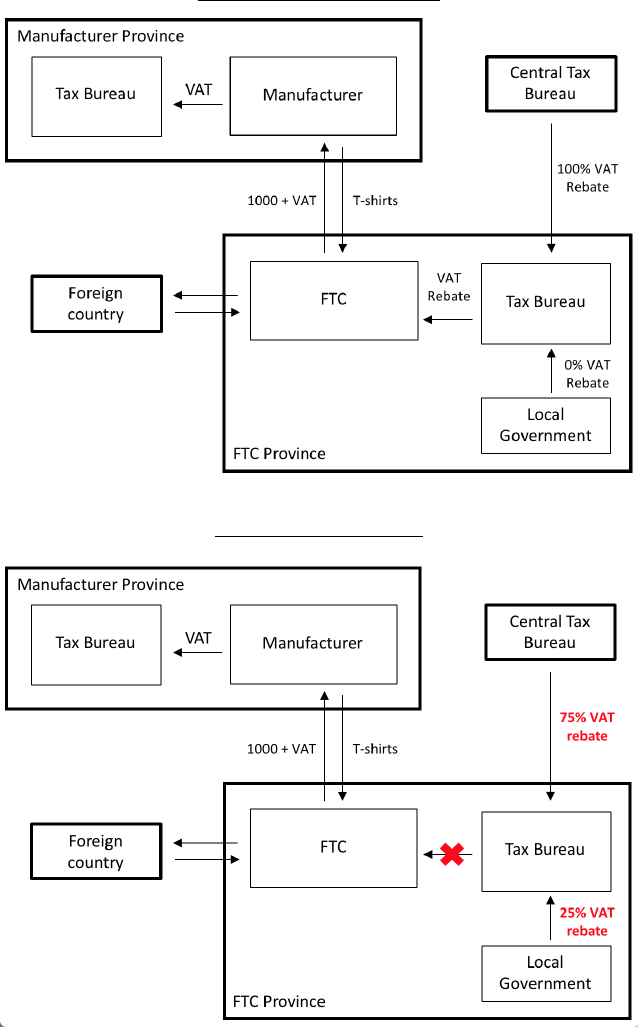

Consistent with the above discussion, many FTCs became more “inward-looking” after the reform

to avoid delays in VAT rebates from their local governments. Figure 2 describes the changes in FTCs’

sourcing patterns before and after the reform. Panel A plots the cumulative distribution function of

the number of sourcing provinces among the FTCs in different years. Panel B examines the fraction of

local goods in total export sales. We see that along both the extensive and intensive margins, the FTCs

had been becoming more outward-looking prior to the reform, but the trend sharply stopped in 2004.

9

While the time-series patterns are consistent with rising local protectionism, many macroeconomic

factors could be at play. Our empirical strategy controls for the aggregate shocks and explores within-

country across-province-industry and across-firm variations for identification (see Section 5).

2.3 Impacts on Manufacturing Exports and Firm Performance

In light of the disruption of the FTCs’ domestic sourcing, upstream manufacturing firms could be ad-

versely affected. Consider a typical manufacturing firm in China. The firm has two ways to export

its products to the international markets, either directly exporting on its own or indirectly exporting

through the FTCs.

10

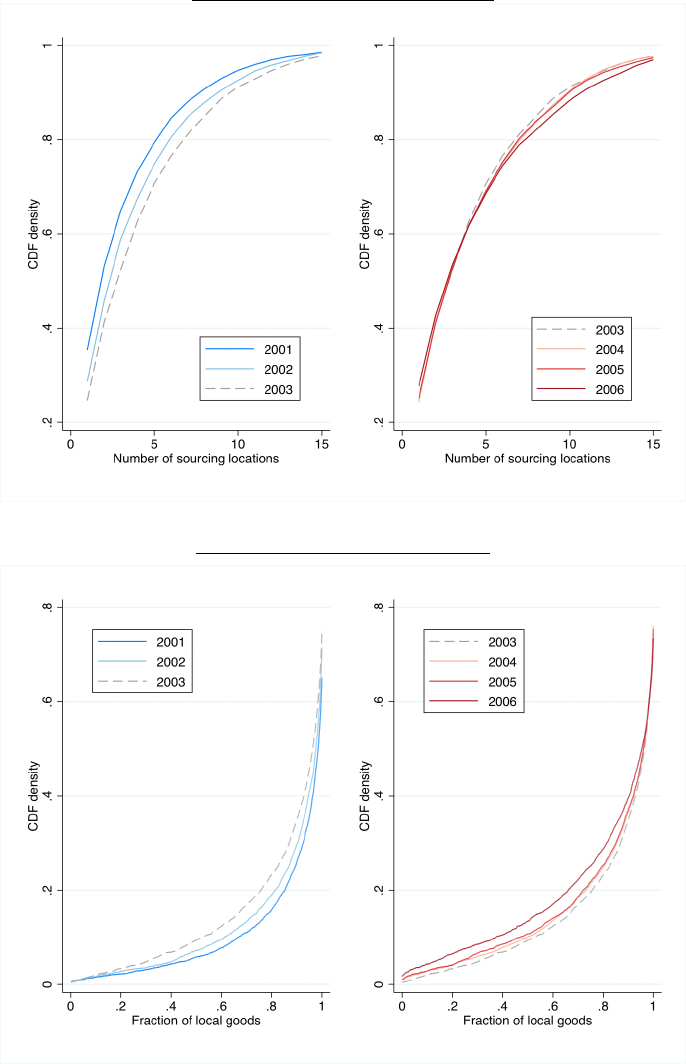

Exporting through FTCs constitutes a significant share of the total export activ-

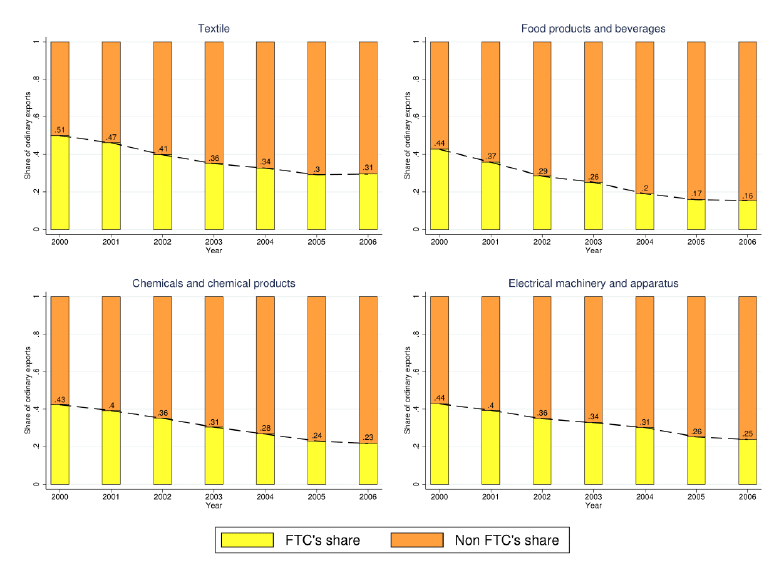

ities in China. Figure 3 shows that a relatively small number of FTCs account for more than 30% of

the country’s total ordinary exports between 2001 and 2006. Figure A.1 shows that FTCs are respon-

sible for large fractions of exports in four major export industries, namely textiles, food products and

8

The Provisions on Prohibiting Regional Blockade in Market Economic Activities enacted in 2001 explicitly forbids

local governments from restricting firms, in any manner, to purchase only the products and inputs that are locally made.

9

The trend picked up again in 2006, which is consistent with the scaling down of the local rebate burden from 25% to

7.5%. In our empirical analysis, we take into account the revision of the sharing rule in constructing the policy shocks and

the results are robust to this adjustment.

10

There are two modes of indirect exporting via FTCs: the first is through formal contracting and the second is direct

selling. The problem with the shifting tax rebate burden arises in the latter case; for the former, the rebate burden always

falls on the province where the manufacturing firm is located. Our study therefore focuses on the second case.

7

beverages, chemicals and chemical products, and electrical machinery and apparatuses.

Due to the high fixed costs of direct exporting, many small and medium enterprises have relied on

FTCs to export (Lin, 2017). This is especially true for manufacturing firms located in inland provinces.

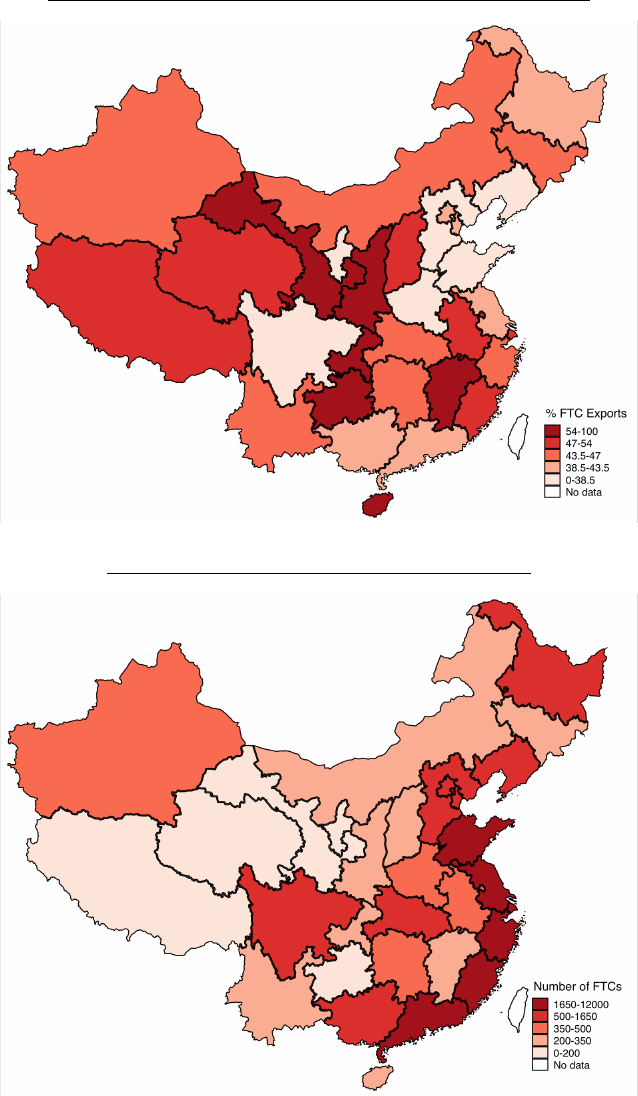

Panel A of Figure 4 shows the distribution of reliance on FTCs as defined by the percentage of a

province’s total exports through FTCs. As the figure shows, many inland provinces heavily depend on

FTCs for exporting. On the other hand, most FTCs are located in the coastal areas, as shown in Panel

B of Figure 4.

11

As a result, small and medium manufacturers in inland regions may be particularly

susceptible to the protectionist practices that suppress non-local sourcing activities of the coastal FTCs.

In principle, the policy could also affect downstream manufacturing firms that source production

inputs from non-local upstream firms. To fully characterize the impact on the domestic supply chain,

one would need information on firm-to-firm transactions. In this paper, we focus on the role of the

intermediary sector and the impact on upstream manufacturing firms by exploring a unique feature of

the Chinese Customs data that allows us to trace the sourcing locations of the FTCs. We describe the

data in more detail in Section 4.

In the next section, we develop a theoretical framework to formalize the discussion above and derive

testable predictions to guide our empirical analysis.

3 Theoretical Framework

The model extends the standard open-economy heterogeneous firm model in Melitz (2003) by adding an

intermediary sector. We model the intermediary technology following Ahn, Khandelwal, and Wei (2011)

but focus on its role in domestic sourcing and the result of impeding such activity. Importantly, we allow

for multiple intermediary technologies with different costs of access, as well as heterogeneous reliance

on these technologies among different provinces in China. This enables us to examine the differential

impact of increasing the costs of “indirect exporting” (i.e., exporting through intermediaries) due to

rising local protectionism on regions with different baseline characteristics. The model generates several

reduced-form predictions that we bring to the data in the next section.

3.1 Basic Setup

Demand Side

Consider two countries, China and the Rest of the World (ROW), and two sectors, one differentiated-

11

Of the 31 provinces, 12 are classified as coastal provinces according to the official Chinese definition: Beijing, Fujian,

Guangdong, Guangxi, Hainan, Hebei, Jiangsu, Liaoning, Shandong, Shanghai, Tianjin, and Zhejiang.

8

good sector and one numeraire-good sector. Consumers in both countries have Cobb-Douglas preferences

over the two sectors. In particular, foreign consumers’ utility can be written as:

U =

A

α

1

A

α

2

, α

1

+ α

2

= 1.

1 2

where A

1

and A

2

are the subutility obtained from numeraire good and differentiated good respectively.

Within the differentiated-good sector, consumers have CES preference over different varieties ω:

Z

σ

σ

σ−1 σ−1 σ−1

σ−1 σ−1

(X

CR

) A

2

= q(ω)

σ

dω =

σ

+ (X

RR

)

σ

ω∈Ω

where X

ij

, for i, j ∈ {(C)hina, (R)OW }, represents the subutility derived from the consumption of

products made in i by consumers in j. Let P

CR

denote the price index of Chinese export in the ROW:

Z

1

P

CR

= p

CR

(ω)

1−σ

dω

1−σ

.

ω∈Ω

CR

Thus, demand from the ROW for variety ω made in China is:

p

CR

(ω)

−σ

X

CR

q

CR

(ω) =

P

CR

Supply Side

Chinese consumers offer one unit of labor and receive a normalized wage of 1 (assuming a freely traded

numeraire good produced by one unit of labor). Firms pay an entry cost of f

E

and draw productivity

φ from a Weibull distribution G(φ). Assuming constant marginal cost, the amount of labor required to

q

produce q units of output is l =

φ

for a firm with productivity φ. The CES demand function implies that

1−σ

1

R

CC

p

D

the optimal price for the domestic market is p

D

= The domestic profits is π

D

(φ) =

1

P

CC

.

ρφ

.

σ

A Chinese firm can access the foreign market by directly exporting on its own or indirectly exporting

through an FTC. For direct exporting, the firm incurs a per period fixed cost f

X

and a per unit

iceberg cost τ . For indirect exporting, the firm chooses among FTCs located in different provinces.

Each province has a perfectly competitive intermediary sector consisting of identical FTCs open to all

provinces. If a firm φ of province i sells its variety through the intermediary sector in province j, it

ij ij

pays a fixed cost f

I

and a per-unit variable cost γ

I

to the FTC but no longer incurs the iceberg cost.

Following Ahn, Khandelwal, and Wei (2011), we assume that the fixed cost of indirect exporting is

ij

lower than that of direct exporting, i.e., for any i and j, f

I

< f

X

.

9

3.2 Solving Firms’ Profit Maximization Problem

The timing is as follows:

1. Entrants pays f

E

to enter the market and draw productivity φ. Low-productivity entrants exit.

2. Surviving firms make production and export decisions: firms choose to stay domestic or serve

both the domestic and foreign markets. Exporters decide on the exporting technology: direct or

indirect exporting, and if the latter, which FTC to use.

3. Prices and quantities are set.

We solve the firm’s problem backward:

Stage 3

Direct exporter φ solves the profit-maximization problem

12

:

1 τ

π

X

(φ) = max π

X

(φ, p

X

) = p

X

q(p

X

) − q(p

X

)τ − f

X

⇒ p

X

(φ) =

p

X

φ ρφ

where p

X

is the price charged to foreign consumers. On the other hand, indirect exporter φ of province

i solves the problem:

ij

∗

ij

∗

ij

∗

1

ij

∗

ij

∗

ij

∗

γ

I

π (φ) = max π (φ, p

I

) = p

I

τq(τp

I

) − τq(τp

I

)γ − f ⇒ p (φ) =

I I I I I

p

I

φ ρφ

where province j

∗

is the profit-maximizing FTC province for firm φ, and p (φ) is the price the firm

I

charges to the FTC in province j

∗

. Since the intermediary sector is perfectly competitive, it passes the

iceberg trade cost by setting the price in the foreign market as τ p

I

. The exporter has to sell to the FTC

quantity τq in order for quantity q to reach the foreign market.

Stage 2

Firms decide

whether to produce and export, and if export, which exporting technology to use. Following

the result above, the profits from direct exporting is:

12

From now on, we abbreviate CR subscript for q

CR

, R

CR

, and P

CR

1−σ

1 τ

π

X

(φ) = R − f

X

.

σ ρφP

ij

∗

10

Similarly, the profits of indirect exporting through the intermediary sector in province j is:

ij

∗

ij

Let π

i

= π , where j

∗

= argmax

j

π .

I

I I

Firms choose the optimal production and exporting technology by solving the following:

1

τγ

ij

1−σ

ij

I

ij

π (φ) = R − f

I I

σ ρφP

π = max{π

I

+ π

D

, π

X

+ π

D

, π

D

}.

Stage 1

Finally

, a firm of province m

φ

decides whether to enter the market by calculating:

Z

E

φ

π(φ) = π(φ)dG(φ) − f

E

φ

3.3 Solving for Productivity Cutoffs of Various Exporting Technologies

Suppose there are M provinces in China. Due to the variation in the fixed and variable costs of

direct and indirect exporting technologies, for every province there is naturally a pecking order of

exporting technology, i.e., a productivity ladder that assigns firms with different productivities into

different optimal exporting technologies. Without loss of generality, suppose that for province i, the

ii

M

productivity cutoffs of indirectly exporting through M provinces are ranked as φ

ii

1

< φ

ii

2

... < φ ,

I I I

where φ

ii

m

denotes the productivity cutoff of indirectly exporting through FTCs in province i

m

, the

I

mth province in the productivity ladder of province i.

13

This leads to an important observation that

f

ii

m

ii

m−1

ii

m−1

> f and γ

ii

m

< γ ∀m ∈ [2, M ].

14

We assume that own province has the lowest fixed

I I I I

cost, and thus the own province is ranked at the last in the productivity cutoff ladder, i.e., i = i

1

.

Furthermore, since f

X

> f

ii

m

, ∀m and direct exporting incurs no additional variable cost, we have

I

φ

ii

m

< φ

X

, ∀m ∈ [1, M], where φ

X

denotes the productivity cutoff of direct exporting.

I

13

Mathematically, there may be a province j that would not be economically viable for indirect exporting by province

ij ij

0

ij ij

0

j

0

if there exists another province j

0

such that f > f and γ > γ . This can rationalize the empirical observations

I I I I

that a province never indirectly exports through another province. However, for tractability here we assume away such

provinces.

14

Suppose that for firms in province m, no two provinces have the same fixed and variable costs of indirect exporting.

ii

m−1

ii

m−1

If f

ii

m

> f and γ

ii

m

> γ , then province i

m

would be strictly dominated by province i

m−1

, and vice versa;

I I I I

ii

m−1

ii

m−1

if f

ii

m

< f and γ

ii

m

> γ , then province i

m−1

would rank above i

m

in the productivity cutoffs of indirect

I I I I

exporting.

11

We can obtain φ

ii

1

I

by setting the profits of indirectly exporting through local province to zero:

(γ

ii

1

1

)

1−σ

1−σ

π

ii

1

(φ

ii

1

⇒ φ

ii

1

I

) = 0, = A

I I I

f

ii

1

I

We can also solve any φ

ii

m

, m ∈ [2, M] from the indifference conditions:

I

1

(γ

ii

m

)

1−σ

− (γ

ii

m−1

)

1−σ

1−σ

π

ii

m

(φ

ii

m

ii

m−1

(φ

ii

m

⇒ φ

ii

m

I I

) = π ), = A

I I I I I

f

ii

m

ii

m−1

− f

I I

Finally, φ

X

can be obtained by equating the profits of exporting directly and the profits of exporting

indirectly through the highest ranked province in the productivity cutoff ladder:

τ

�

R

1−σ

where A = .

ρP σ

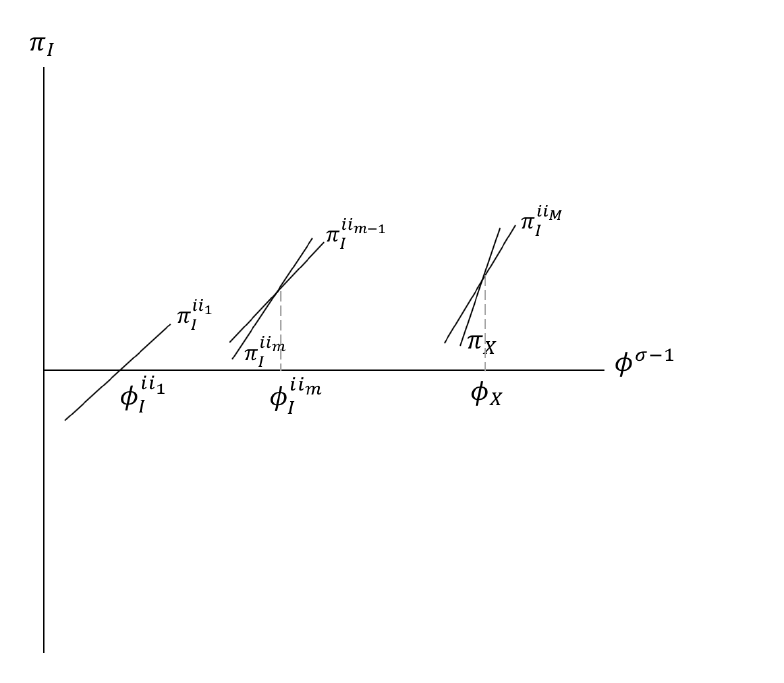

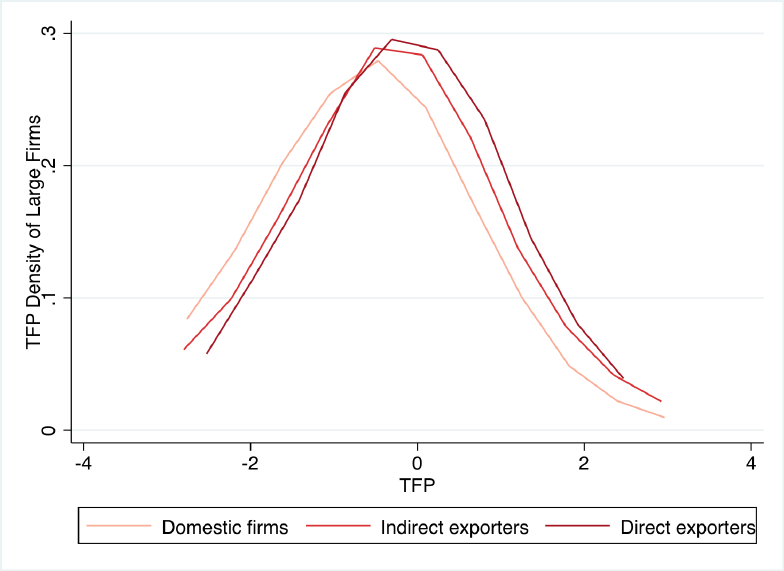

Figure A.3 illustrates the productivity cutoffs. One of the immediate implications from the discus-

sion above is that the most productive firms will be direct exporters, followed by indirect exporters,

and the least productive firms will serve domestic market only. We verify this pecking order in the

Chinese context: Figure A.4 plots the empirical TFP distribution of the three groups of firms, and the

patterns are largely consistent with the theoretical prediction, showing a rightward shift in productivity

distribution as we move from non-exporting firms to indirect and direct exporters.

15

1 − (γ

ii

M

)

1−σ

1

I

π

X

(φ

X

) = π

ii

M

(φ

X

), ⇒ φ

X

= A

1−σ

I

f

X

− f

ii

M

I

3.4 Testable Predictions

After the policy reform, a greater fraction of the tax rebate burden falls on the provincial government,

leading to rising local protectionism that hinders the non-local sourcing activity of the intermediary

sector. To map the empirical context into the model, we consider an increase in the costs of indirect

exporting through non-local intermediaries; the bigger the rebate burden (proxying a local government’s

incentives to block non-local trade), the greater the increase. For simplicity, we assume that the cost

of the protectionist measures passes through the variable cost of indirect exporting. We state the

15

We follow Olley and Pakes (1996) and Brandt, Van Biesebroeck, Wang, and Zhang (2017) to estimate the TFP of

the Chinese manufacturing firms. The TFP used in the plot is demeaned by province and industry. Because the export

volume in the Customs Database is direct exports and that in the NBS survey is total exports, we define domestic firms as

the ones that have zero exports in both datasets, indirect exporters as the firms which have positive exports in the NBS

survey but zero exports in the Customs Database, and direct exporters as the ones whose share of direct exports among

total exports are more than 0.9 (∼ the 90th percentile in the sample).

12

assumption formally below:

Assumption 1. Let c denote a measure of the tax rebate burden falling on the provincial governments.

ii

m

ii

m

ii

m

dγ dγ df

I I I

For any province i, > 0 if i

m

6= i, = 0 if i

m

= i, and = 0 ∀m ∈ [1, M],

dc dc dc

In principle, both the fixed costs and variable costs of indirect exporting may be affected. We derive

the predictions based on an increase in the variable costs, and all the results are qualitatively robust

for an increase in the fixed costs.

dP

CR

Assumption 2.

dc

= 0.

We abstract away from general equilibrium effects and focus on partial equilibrium predictions. Our

reduced form analysis explores subnational variations in rebate burdens and exposures to the reform,

controlling for aggregate time shocks.

16

Below, we derive five predictions on Chinese firms’ exporting behavior as a result of the rebate

burden and an increase in the costs of indirect exporting. Details of the proofs are in Appendix C.

Prediction 1. The number and the export volume of direct exporters increase in c.

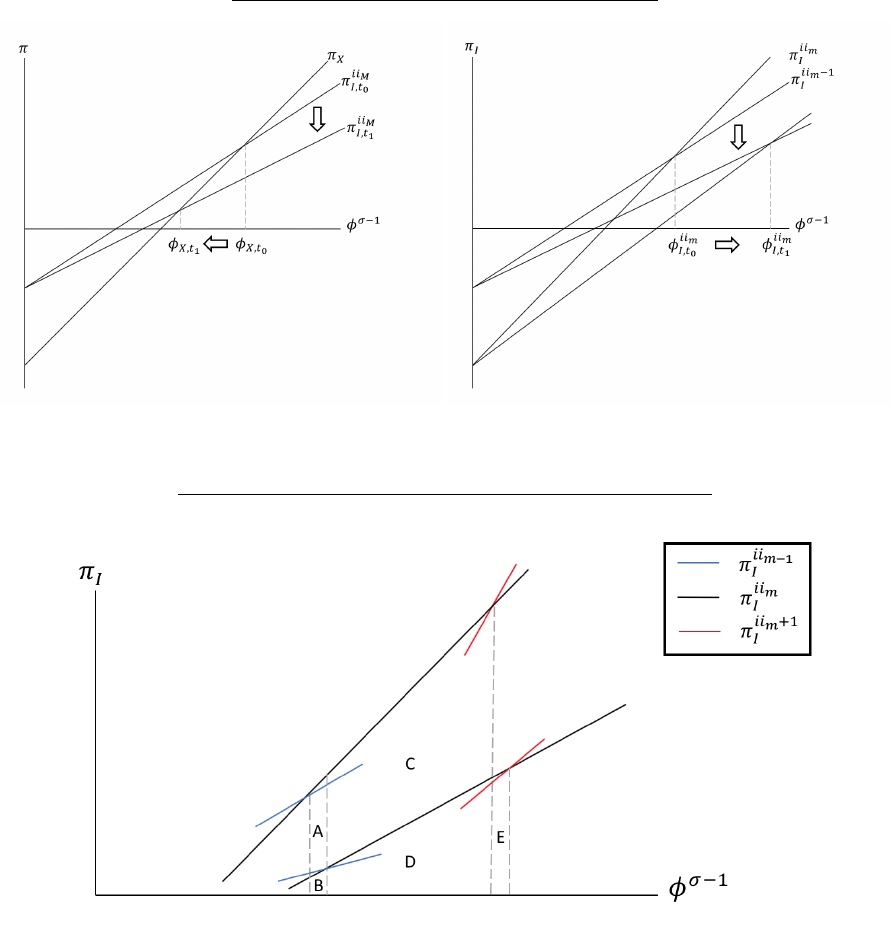

Plot (a) in Panel A of Figure 5 illustrates how the number and the export volume of direct exporters

respond in response to an increase in c. For province i, as c increases, the variable cost of indirect

exporting increases through every non-local province, including province i

M

, the highest province in the

productivity cutoff ladder of indirect exporting. Therefore, some firms that were previously exporting

through the FTCs in province i

M

would switch to direct exporting, resulting in a leftward shift of the

productivity cutoff of direct exporting φ

X

and an increase in the volume of direct exporting.

Prediction 2. For each province, the number of indirect exporters decreases in c. The indirect exporting

volume also decreases in c if the productivity cutoffs increase across all indirect exporting technologies.

As c increases, the profits of indirect exporting through all provinces decrease, shifting up the

productivity cutoff between staying domestic and indirect exporting. Combined with Prediction 1,

[φ

ii

1

I

, φ

X

] shrinks and the number of indirect exporters decreases. However, the impact on the total

indirect exporting volume is theoretically ambiguous. This is because firms can switch to different

provinces for indirect exporting after the reform, depending on how much more costly it becomes to

access an intermediary sector in a given province. It could be that a firm switches to a province with

higher fixed cost but lower variable cost compared to what it has used before, in which case the firm’s

16

dγ

dP

CR

The theoretical results hold under a more general condition that > .

dc dc

13

(indirect) export volume would actually increase. On the other hand, if all the productivity cutoffs shift

to the right among the set of viable indirect exporting technologies, as illustrated in plot (b) in Panel

A of Figure 5, the indirect export volume would fall.

17

Next, we examine how domestic trade along different indirect exporting routes, from manufacturing

firms in a given province to the intermediary sector in another province, is distorted. Let R

ii

m

denote

I

the total indirect exporting volume flowing from province i to its mth ranked FTC province in the

productivity cutoff ladder prior to the reform:

Z

ii

m+1

φ

I

R

ii

m

ii

m

I

= r

I

(φ)dG(φ).

φ

ii

m

I

After the reform, with an increasing local tax rebate burden, we can show that:

(1)

Z

ii

m+1

1−σ

φ

ii

m+1

∂R

ii

m

I

∂r

ii

m

(φ) τγ

ii

m

�

∂Θ(φ ) ∂Θ(φ

ii

m

)

I I I I I

= dG(φ) + R × −

∂c

ii

m

∂c ρP ∂c ∂c

φ

I

| {z }

| {z }

Network effect; ambiguous sign

Price effect; ≤0

R

φ

where Θ(φ) = φ

0σ−1

dG(φ

0

). This equation decomposes the effect of increase in c on R

ii

m

into two

−∞

I

parts: the price effect and the network effect. The price effect captures the change in R

ii

m

if indirect

I

exporters in i continue to export through the same provinces. The effect channels through the effect of

c on p

I

and the response of foreign demand to the change of prices. On the other hand, the network

effect captures switchings among different indirect exporting routes: indirect exporters of province i

may cease to export through province i

m

or they may shift more trade to i

m

, depending on how the

other routes are affected. Panel B of Figure 5 illustrates the two effects graphically. Given that it takes

time to look for new intermediaries and re-optimize among the indirect exporting routes, in the short

run, one may expect that the price effect outweighs the network effect, as shown in the case of Panel B.

Prediction 3. Given an increase in c, for any province i: (1) local exporters rely more on local FTCs

after the reform, i.e., the number and the export volume of indirect exports through local FTCs increase

in c; (2) the indirect export volume through other provinces decreases if the price effect outweighs the

network effect (as defined in Equation (1)).

Finally, we examine heterogeneity across provinces based on their exposure to the reform, and map

these predictions to the data. Let B

ij

denote the percentage change of the variable cost of indirectly

dγ

I

ij

/dc

exporting from province i through j with respect to a change in c, i.e., B

ij

=

ij

. We can define a

γ

I

17

A sufficient condition is that for any province i, dγ

ii

m

/dc > dγ

ii

n

/dc, ∀m, n s.t. γ

ii

m

< γ

ii

n

before the reform.

I I I I

14

province i’s exposure to the reform:

Definition 1. The exposure of province i to an increase in c, denoted as E

i

, is the sum of the percentage

change in variable costs of indirect exporting through all provinces from province i, weighted by the

share of indirect export volume through each province:

X

R

ii

m

E

i

≡ B

ii

m

ω

ii

m

ω

ii

m

I

, where =

P

I I

R

ii

n

m∈[1,M]

n∈[1,M]

I

In

tuitively, a pro

vince is more “exposed” to the reform if it relies more on intermediaries in provinces

with larger increase in the variable cost of indirect exporting.

Prediction 4. If the price effect is sufficiently larger than the network effect, given an increase in c,

indirect export volume from province i decreases more through provinces with larger B

ij

.

Prediction 5. If the price effect is sufficiently larger than the network effect, given an increase in c, a

province with higher exposure E will experience a larger percentage decrease in indirect exports.

4 Data

4.1 Chinese Customs Database

Our main data set is the Chinese Customs Database, which provides transaction-level trade flows

information on the universe of China’s exports and imports. For this study, we focus on exports

during the time period between 2001 and 2006.

18

The data is collected and made available by the

Chinese Customs Office. For each transaction, we observe the exporting firm identity, ownership type

and location, trade type, value and quantity of the exports, 8-digit HS code, city in China where the

product is manufactured (i.e., the origin location), customs office where the transaction is processed

and the final destination. The origin location information is a unique feature of the Chinese data that

is typically not present in other Customs databases. Conversations with officials from the Chinese

Customs office revealed that the collection of this information is required by the State Administration

of Taxation, for the purpose of cross-validating the VAT receipts for tax rebate.

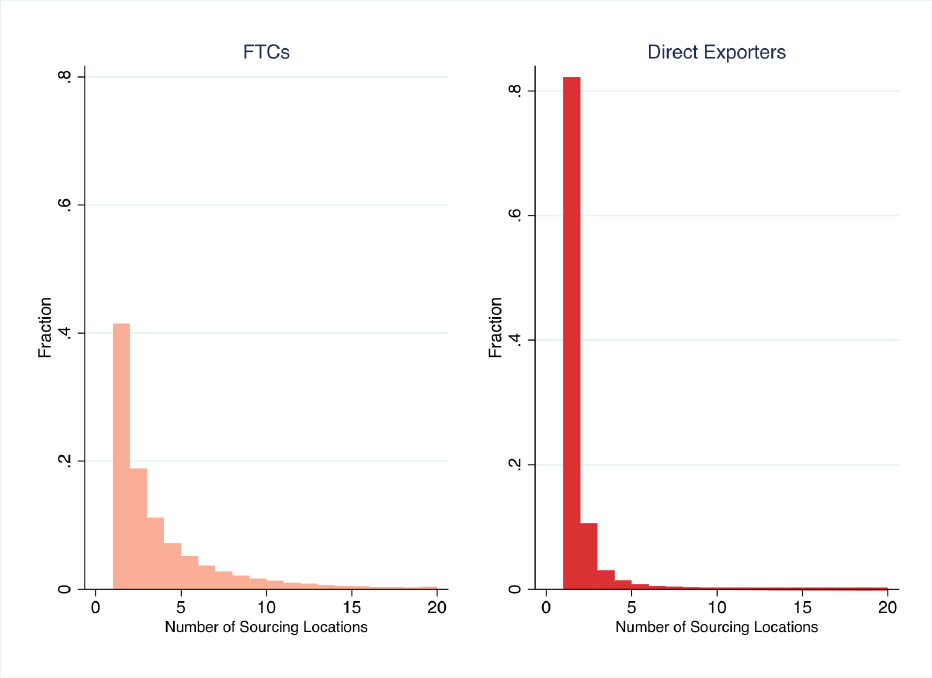

To examine the behavior of FTCs, we follow the strategy in Manova and Zhang (2009) to identify

the set of FTCs based on Chinese characters that have the English-equivalent meaning of “importer”,

18

China entered WTO in 2001.The data after 2006 is no longer at the “transaction” level, and thus does not allow one

to identify the origin location of each export transaction.

15

“exporter”, and/or “trading” in their firm name.

19

This classification is not perfect as there can be

both inclusion and exclusion errors.

20

As a first pass, Figure A.2 plots the sourcing patterns of FTCs

and non-FTCs using the pooled data from 2000 to 2006. Reassuringly, we see that on average, FTCs

source from more provinces than non-FTCs. Not surprisingly, most (80%) non-FTCs export products

that come from a single province–the province in which the exporting firm is located. In other words,

these are manufacturing firms that produce and export on their own. Panel A of Table 1 presents the

summary statistics of FTCs in the pre-reform baseline year 2003.

4.2 NBS Survey of Manufacturing Firms

To examine the impact of local protectionism on manufacturing firm performance, we merge the Customs

data with the NBS annual survey of manufacturing firms.

21

The annual survey is conducted by the

National Bureau of Statistics (NBS), and it includes all industrial firms that are identified as being

either state-owned or non-state firms with sales revenue above 5 million RMB. As discussed in Brandt,

Biesebroeck, and Zhang (2012), even though a large number of firms (80%) are excluded from the

sample, they account for only a small fraction (9.3%) of the total economic activities in China.

22

Panel

B of Table 1 presents the summary statistics of the balanced sample of manufacturing firms (i.e., 57,301

firms that appear in all 6 years in the data from 2001 to 2006).

23

One important variable in the NBS data is a firm’s total export revenue. Compared to the export

sales captured in the Customs data, which only reflects a firm’s direct exports, the self-reported amount

in the NBS data presumably captures both direct exports and indirect exports through FTCs. In

principle, we can derive a firm’s indirect export revenue by subtracting the two numbers. One concern

with this approach is reporting noise, especially if firms consider some of their sales to FTCs as domestic

sales rather than “exports”. We address this concern in our empirical analysis (see Section 6.4).

19

In pinyin (Romanized Chinese), these phrases are: jin4chu1kou3, jing1mao4, mao4yi4, ke1mao4 and wai4jing1.

20

As noted in Khandelwal, Schott, and Wei (2013), some state-owned manufacturers may export through trading arms

of their production facilities under a name that contains phrases such as importer, exporter and trader.

21

We follow the standard procedure and link firms by their names following Yu and Tian (2012). We improve on the

previous procedure by first standardizing firm names in both datasets.

22

Trade in services accounts for a small fraction of the total trade activities during this period. We follow the industry

concordance constructed by Brandt, Biesebroeck, and Zhang (2012) to ensure a coherent classification over time.

23

There is a sharp increase in the number of firms in the sample between 2003 and 2004 as a result of the 2004 Industrial

census—many firms above the 5 million RMB cutoff should have been in the sample in earlier years, but had been left

out due to issues with the business registry. To avoid the composition change, we focus on a balanced sample of firms. A

comparison between the balanced sample and the unbalanced sample can be found in Table B.1.

16

4.3 Export VAT Rebate Rates

We compile a comprehensive list of export VAT rebate rates at 10-digit HS product code from 2001 to

2006 based on official announcements released by the Chinese government.

24

We aggregate the rebate

rates to 6-digit HS code by taking arithmetic averages (rebate rates within a 6-digit code are usually

identical). Panel C of Table 1 describes the distribution of rebate rates across 6-digit HS industries

in 2003. Over 80% of goods have a rebate rate of 13%; others categories include 0%, 5%, 10%, and

17% (full rebate). Section 5.1 describes how we use the rebate rates to construct measures of predicted

rebate burden for local governments under the new policy.

4.4 Provincial Statistical Yearbooks

The Provincial Statistical Yearbooks provide basic macroeconomic statistics for 31 provinces in mainland

China. Panel D of Table 1 presents basic summary statistics for the year 2003. We use information on

government revenue and expenditures to construct various proxies for local fiscal capacity. We expect

that the higher the predicted rebate burden as a share of local fiscal capacity, the stronger the incentive

of the local government to discourage non-local sourcing to alleviate the rebate burden.

25

5 Empirical Strategy

This section describes the empirical strategy to test the predictions in Section 3. We focus on Prediction

4 and 5, which guide us to exploit subnational variations and employ a difference-in-difference strategy

for identification. Section 5.1 and 5.2 describe how we measure the rebate burden and exposure to

reform. Section 5.3 describes the empirical specifications for examining the impact on interprovincial

trade, sourcing patterns of FTCs, and exporting activities of manufacturing firms.

5.1 Predicted Rebate Burden

For each province, we compute a measure of predicted rebate burden based on local intermediaries’

pre-reform trading patterns and rebate rates across industries. Specifically, we calculate the amount of

VAT rebates each province would have to pay out due to its local FTCs’ non-local businesses for each

24

Export VAT rebate rates are published on the government website http://www.gov.cn/fuwu/chaxun/cktsl.html.

25

One caveat is that certain extra-budgetary sources of revenue are off the book (for example, money from selling lands,

which is known to be an important source of revenue for local governments in China). However, such information has

been poorly documented. To the extent that the different sources of revenue may be correlated, we perform a series of

robustness checks using various measures that are available.

17

post-reform year had the non-local trading volume stayed the same as the pre-reform period. We scale

the predicted rebate amount by a province’s fiscal capacity, measured by total government revenue, to

capture the degree of fiscal stress induced by the policy change.

26

Formally,

6

P P

ij

s∈S

0.25 × ι

st

× R

B

ˆ

j

i=j

I,s

= , for t ≥ 2004

t

G

j

where s is 6-digit HS code and S is the universe of export products

27

; ι

st

is the VAT rebate rate of sector

P

ij

s in year t; R is the sum of average indirect export volume from other provinces through j for

=j

the three years before the reform; G

j

indicates the average total government revenue of province j in

the pre-reform period. 0.25 is the rebate share borne by the provincial government after the reform.

28

i6

I,s

j

ˆ

B

t

= 0 for t < 2004.

Conceptually, we expect that the higher predicted rebate burden would lead to a stronger incentive

to discourage non-local sourcing and consequently to greater costs of accessing the local intermediary

B

ˆ

j

sector. Therefore, is a reduced-form way of capturing the cost shocks to the indirect exporting

t

dγ

I

ij

/dc

technology as a result of increasing c, mapping to B

ij

=

ij

in the model.

γ

I

Table 2 shows substantial variations across Chinese provinces in terms of the predicted rebate

burden.

29

An important part of the heterogeneity is coming from variations in baseline sourcing patterns

of the local FTCs, particularly the average non-locally sourced exports between 2001 and 2003.

5.2 Exposure to Reform

Next, we use the predicted rebate burden to construct a measure of reform exposure for each province.

The idea is that a province that relies more on FTCs in provinces with larger predicted rebate burden

would be more exposed to the reform in light of the greater protectionist incentives of other provinces.

Mathematically, following Definition 1 in the model, we construct the exposure measure as weighted

sum of the rebate burden:

X

E

ˆ

i

B

ˆ

i

m

ω

ii

m

= ˆ

t

t

I

m∈[1,M]

(2)

26

In the robustness checks, we consider alternative measures of fiscal capacity, including total tax revenue, VAT revenue,

and rollover balance, and obtain very similar results.

27

Throughout the paper, we use s to denote 6-digit HS code, S 2-digit HS code, and S the universe of export products.

28

There was a subsequent revision of the sharing rule after 2005, which changed the rebate share falling on the provincial

government to 0.075. In the robustness checks, we take into account the subsequent revision of the policy in constructing

the predicted rebate burden.

29

The complete list of predicted burdens in 2004 for each province can be found in Table B.2.

18

ii

R

m

where ωˆ

ii

m

=

P

I

ii

is

I

the average pre-reform share of indirect export volume of province i through

R

n

n

I

i

m

. It captures i’s baseline reliance on export intermediaries in other provinces.

Table 2 shows meaningful variations in reform exposure across provinces.

30

This is primarily driven

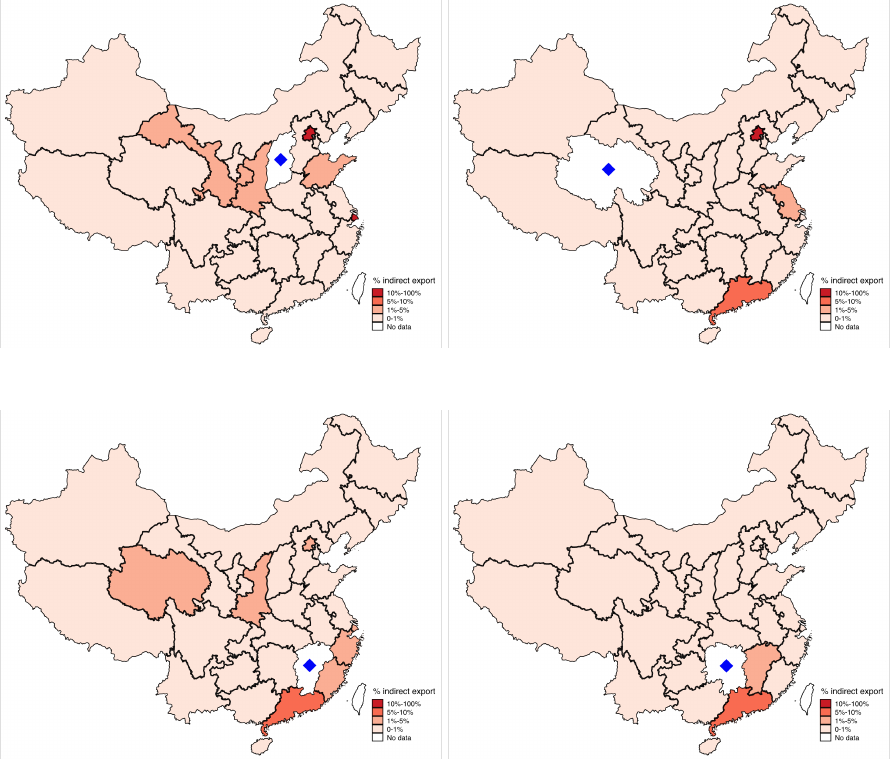

by heterogeneity in indirect exporting choices at baseline. Figure 6 illustrates the cases for four provinces:

two northern provinces, Shanxi and Qinghai, and two southern provinces, Jiangxi and Hunan. For the

two northern provinces, most of their indirect exports in 2003 were through FTCs in the northern

coastal provinces. The opposite is true for the two southern provinces, suggesting that distance matters

for domestic trade.

Analogously, we can define the exposure measure at province-industry (2-digit HS code) level:

X

E

ˆ

i

B

ˆ

i

m

ω

ii

m

= ˆ

St

t

I,S

m∈[1,M]

ii

R

m

where ωˆ

ii

m

I,S

I,S

=

P

ii

is the average pre-reform share of indirect exports of industry S in province i

R

n

n

I,S

that are through the intermediary sector of i

m

. This allows us to exploit finer subnational variations

for identification. We now turn to describe our empirical specifications in detail.

5.3 Empirical Specifications

5.3.1 Impact on Interprovincial Trade

Prediction 4 says that indirect export volume from province i would decrease more through provinces

with larger rebate burden. To examine this, we look at interprovincial trade flows and exploit hetero-

geneity in the predicted rebate burden of the downstream province:

(3)

ij

B

j

R = α + β

ˆ

+ ν

ij

+ λ

t

+ κ

i

Year + κ

j

Year + θ

1

ι

it

+ θ

2

ι

jt

+

ijt

It

t

The dependent variable is the total amount of indirect exports that originated from province i and were

exported through FTCs in province j. The key regressor is j’s predicted rebate burden in year t. Our

baseline regression controls for province-pair FE ν

ij

, year FE λ

t

, and province-specific linear time trends

for both provinces. Standard errors are clustered at the province-pair level.

This corresponds to a difference-in-difference specification. The key assumption for identification is

that without the reform, the average change in export volume would have been the same across each

30

The complete list of exposure measures in 2004 for each province can be found in Table B.2.

19

indirect exporting route. To examine this assumption, we check the correlations between the predicted

rebate burden with a rich set of provincial pre-reform characteristics, both in terms of the baseline level

and the growth rate.

31

The results, shown in Table B.3, are reassuring. Our main results in Section 6

are robust to controlling for these variables and their interactions with time (not shown).

One potential confounding factor is changing industrial rebate rates over time, which may be cor-

related with both the predicted rebate burden and the volume of indirect trade. To address this, we

further control for the average rebate rates faced by provinces i and j given their baseline export mix,

denoted as ι

it

and ι

jt

in Equation (3).

32

5.3.2 Impact on the Sourcing Patterns of FTCs

A

direct implication of Prediction 4 is that FTCs in provinces with a greater rebate burden would

become more “inward-looking” in terms of their sourcing behavior. To examine this, we run the following

difference-in-difference regression at the firm level:

(4)

Y

ft

= α + β B

ˆ

j

+ ν

f

+ λ

t

+ κ

j

Year + θι

jt

+

ft

t

where the outcome variables include exports sourced from local and non-local manufacturers, as well

as the share of exports sourced from local manufacturers by FTC f of province j at year t. The key

j

ˆ

regressor of interest is B , the predicted rebate burden of province j in which f is located. We control

t

for firm FE ν

f

, year FE λ

t

, province-specific linear time trends, and the average rebate rate faced by

m

f

. Standard errors are clustered at the province level.

33

31

The variables we examine include the baseline levels and the growth rates of provincial government revenue, balance,

tax revenue, value-added tax, GDP, population and the baseline levels of total provincial exports, direct exports, indirect

exports, number of FTCs, and number of exporting firms.

32

The average rebate rate faced by province i is constructed as the average rebate rates of industries weighted by their

pre-reform value shares in the total exports the province manufactures:

X

01−03

i’s total exports of s

ι

it

= ι

st

× .

s∈S

i’s total exports

01−03

The average rebate rate faced by province j is constructed as the average rebate rates of industries weighted by their

pre-reform value shares in total indirect exports through j:

P

X

r

ij

i

s

ι

jt

= ι

st

×

P P

ij

s∈S

v

r

v∈S i

33

In total, there are 31 provinces. All the main results in Section 6 are robust to using bootstrapped standard errors.

20

5.3.3 Impact on Manufacturing Exports

To examine the impact of local protectionism on manufacturing exports, we test Prediction 5 by using

the empirical exposure measure E

ˆ

i

described in Section 5.2:

St

(5) Y

i

= α + β E

ˆ

i

St

+ ν

i

+ µ

S

+ λ

t

+ κ

i

Year + θι

iSt

+

iSt

St

where the outcome variables include total exports and indirect exports originated from province-industry

iS in year t. The regression controls for province FE, industry FE, year FE, and province-specific linear

time trend. As discussed above, we further control for the time-varying average rebate rate at the

province-industry level.

34

Standard errors are clustered at the province level.

35

The identification assumption is that without the reform, the average change in export volume would

have been the same across each province or province-industry. Table B.4 examines the correlations

between the province-level exposure measure with a rich set of provincial pre-reform characteristics,

both in terms of the baseline level and the growth rate. The main results in Section 6 are robust to

controlling for these variables and their interactions with time (not shown).

5.3.4 Impact

on Manufacturing Firms

Finally,

we examine the impact on manufacturing firms in terms of their performance and exporting

behavior using the firm-level annual NBS survey data. As discussed in Section 4.2, we can compute a

firm’s indirect exporting volume by comparing the export revenue reported in the NBS data and that

registered in the Customs data. Using this information, we can measure a firm’s baseline reliance on

indirect exports, IndirectDependence, as the fraction of indirect exports over total exports in the pre-

reform period. We focus on the sample of manufacturing firms with positive export volume at baseline

(either direct or indirect). A simple difference-in-difference regression examines the differential impact

of the reform on firms with varying degrees of baseline reliance on indirect exports:

Y

φt

= α + βIndirectDependence

φ

× Post

t

+ ν

φ

+ λ

t

+ κ

i

Year + θι

it

+

φt

(6)

34

The average rebate rate of industry S (2-digit HS) in province i at year t is constructed analogously to ι

it

in Footnote

32 as the average rebate rates of exports weighted by the pre-reform value share in total exports of industry S in province

i :

X

01−03

i’s total exporexportst of s

ι

iSt

= ι

st

× .

s∈S

i’s total exports of S

01−03

35

When the dependent variable is total exports, we modify the empirical exposure measure to more closely capture the

reform’s potential effect on total exports. In particular, the weight in Equation (2) becomes the pre-reform value share of

indirect exports over total exports.

21

E

i

E

ˆ

i

Y

φt

= α + β

1

IndirectDependence

φ

×

ˆ

St

+ β

2

St

+ ν

φ

+ λ

t

+ κ

i

Year + θι

ist

+

φt

where the outcome variables include direct and indirect export revenue, dummies for direct and indirect

exporting, and total sales (including domestic sales) of firm φ in province i at year t. The key regressor

is the interaction between firm φ’s baseline reliance on indirect exports and the post-reform dummy,

which equals to 1 for t ≥ 2004. λ

t

and ν

φ

are year and firm fixed effects. The regression further controls

for the province-specific linear time trend and average rebate rate. Standard errors are clustered at the

province level.

We could replace the post-reform dummy with the reform exposure measure:

(7)

The

same framework also allows us to examine the heterogeneous impact across different types of

firms. In light of a negative shock on the indirect exporting technology, firms that face greater challenges

of switching to direct export would be more adversely affected. We examine the heterogeneity across

firms in Section 6.4. Last but not least, as discussed in Section 4.2, one caveat of the IndirectDependence

measure is that firms may not report all indirect exports in the NBS survey. In other words, some of the

“non-exporters” in the NBS data could well export through FTCs. We return to this point in Section

6.4 after presenting the main results.

6 Results

6.1 Impact on Interprovincial Trade

We begin by examining the impact of increasing provincial rebate burden on interprovincial trade flows

of indirect exports, following the empirical specification in Equation (3).

Results are shown in Table 3. Columns 1 and 2 show that increasing the predicted burden of a

province reduces the amount of indirect exports from other provinces, consistent with Prediction 4.

At the same time, the value share of indirect exports from other provinces via the local intermediary

sector decreases, as shown in Columns 3 and 4, and so does the number of FTCs engaging in non-

local sourcing, as shown in Columns 5 and 6. Based on the coefficient estimate in Column 2, we

can compute the elasticity of interprovincial trade flows of indirect exports with respect to provincial

rebate burden, which equals to 1.15.

36

This implies that an increase in a province’s rebate share from

36

Given that the indirect exports dependent variable in Section 5.3.1 is under inverse hyperbolic sine transformation,

√

R

2

+1

It

the elasticity is calculated as ξ = β × B

t

i

× ≈ βB

t

i

. We use the 2004 provincial average predicted burden as an

R

It

empirical equivalent for B

t

i

.

22

25% to 30% would lead to a reduction of 23% of indirect exports from other provinces through the

local intermediary sector.

37

The magnitude is around 30% of existing elasticity estimates in the trade

literature with respect to physical transportation costs, suggesting that political barriers due to local

protectionism can act as important frictions in domestic trade.

38

Table B.5 shows the results using alternative measures of predicted burden. Table B.6 measures

predicted rebate burden accounting for the revision of the sharing rule in 2005. The results are robust.

6.2 Impact on the Sourcing Patterns of FTCs

Next, we examine how increasing provincial rebate burden affects the sourcing patterns of the FTCs.

Table 4 presents the results following the empirical specification in Equation (4). Consistent with the

results at the interprovincial level, Columns 1 and 2 show that increasing rebate burden decreases the

volume of indirect exports from non-local manufacturers. The magnitude of the estimated coefficient in

Column 2 implies that increasing local rebate share from 25% to 30% would decrease a local FTC’s non-

local sourcing by 12%.

39

This captures the intensive-margin effect, i.e., conditioning on still engaging

in non-local sourcing, comparing to the 23% reduction of total non-local indirect exports in Section 6.1,

which captures both the intensive-margin and extensive-margin effects.

Columns 3 and 4 examine the impact on local goods. While negative, the impact is much less

pronounced compared to non-local goods (Column 4 versus Column 2). Together, these results imply

that the FTCs become more inward-looking after the reform: the share of local goods increases as firms

shift their sourcing activities away from non-local manufacturers, as shown in Columns 5 and 6.

The results using different measures of the predicted rebate burden are presented in Table B.7 and

Table B.8. The results are robust to the alternative definitions.

6.3 Impact on Manufacturing Exports

Given that exporting through non-local FTCs constitutes an important exporting channel for Chinese

manufacturers (Figure 4), we next turn to examine the impact of increasing local trade barriers on man-

ufacturing exports, exploiting variations in the exposure to the reform across provinces and industries.

Table 5 shows the regression results, following the specification in Equation (5). Columns 1 and

2 show that exports of a province-industry is negatively affected by its exposure to the reform. The

37

Using the estimated elasticity, we can compute the effect as (

0.3−0.25

× 100%) ×

ˆ

ξ = −23%.

0.25

38

Recent papers such as Bernard, Eaton, Jensen, and Kortum (2003) and Eaton, Kortum, and Kramarz (2011) use

firm-level data and estimate trade elasticity in the range of 3.6 to 4.8.

39

The calculation follows the same procedure explained in Footnote 36 and 37.

23

magnitude of the estimated coefficients implies that increasing the VAT rebate share from 25% to 30%

would decrease total exports of a given province-industry by 4% and decrease indirect exports by 6%.

40

Results using alternative exposure measures (based on different measures of predicted rebate burden)

are presented in Table B.9 and Table B.10. Results are robust.

6.4 Impact on Manufacturing Firms

Finally, we delve into the level of individual manufacturers and examine how their production and

exporting activities are affected by the reform based on their reliance on indirect exporting prior to the

reform. We focus on the sample of exporting firms at baseline.

41

Columns 1 and 2 of Table 6 report

the regression results of estimating Equations (6) and (7). The results indicate a substitution pattern

from indirect export to direct export among Chinese manufacturers after the reform.

42

The coefficient

estimates in Panel A imply that, with a median exposure in the year after the reform, a firm with a

10 percentage point higher baseline dependence on indirect exporting would experience a 20% greater

reduction in indirect exports and a 9% increase in direct exports.

43

Alternatively, for a firm with a

median baseline dependence on indirect exporting (among exporters), increasing the local government’s

VAT rebate share from 25% to 30% would decrease indirect exports by 7% and increase direct exports

by 4%.

44

Despite the substitution, Column 3 shows that firms with a greater baseline dependence on

indirect exporting experience a greater reduction in total exports after the reform, especially if they

are located in provinces with greater exposure to the reform. Columns 4 and 5 examine the extensive

margin responses, and the results are consistent with the above. Results using alternative exposure

measures (based on different measures of predicted rebate burden) are presented in Table B.11.

Next, we investigate the heterogeneous impact across firms. Given that firms may switch to direct

exporting when indirect exporting becomes more expensive, those who can more easily switch would be

less affected. Given the relatively high fixed costs of direct exporting, the switchers are more likely to

40

The calculation follows the same procedure explained in Footnote 36 and 37.

41

Exporting firms are defined as firms with positive export value reported in the NBS survey between 2001 and 2003.

Results on non-exporters are shown in Table B.12. We see that the impact of the reform mostly falls on the exporters. In

principle, the non-exporters could be affected via local general equilibrium effects.

42

Since more than 75% of existing exporters sell more than 97% of their exports indirectly prior to the reform as shown

in Table 1, the majority of firms experienced a decrease in indirect exports and an increase in direct exports when we take

into account the main effect of exposure and the interaction effect (Panel A of Table 6).

43

Since direct and indirect exports are generally large in value, when taken inverse hyperbolic transformation, we have

p

ln(y + y

2

+ 1) ≈ ln(y)+ln(2). Therefore, the fraction change in y given a change in the dependence on indirect exporting

β

1

×

ˆ

E×ΔIndirectDependence

− 1. can be calculated as

y

1

− 1 = e

y

0

44

Analogous to the previous footnote, the fraction change in y given a change in the exposure can be calculated as

y

1

β

1

×Δ

ˆ

E×IndirectDependence+β

2

×Δ

ˆ

− 1 = e

E

− 1.

y

0

24

be firms with good access to credit and/or sufficient working capital. We consider two proxies, namely

ownership type and baseline size. It has been well documented that in the Chinese context, state

owned enterprises (SOEs) enjoy easier access to bank credit than private firms (e.g

˙

, Song, Storesletten,

and Zilibotti (2011)). To examine the heterogeneity, we add a triple interaction term to our main

specifications in Equations (6) and (7):

(8)

(9)

Y

φt

= α + β

1

IndirectDependence

φ

× Post

t

+ β

2

IndirectDependence

φ

× Post

t

× z

φ

+ β

3

Post

t

× z

φ

+ ν

φ

+ λ

t

+ κ

i

Year + θι

it

+

φt

Y

φt

=

St

+ β

2

IndirectDependence

φ

× E

ˆ

i

α + β

1

IndirectDependence

φ

× E

ˆ

i

St

× z

φ

+ β

3

E

ˆ

i

E

ˆ

i

St

+ ν

φ

+ λ

t

+ κ

i

Year + θι

it

+

φt

St

× z

φ

+ β

4

where z

φ

indicates: (1) a dummy of being a SOE, defined using a firm’s registered capital share, and

(2) log baseline average annual output.

Table 7 reports the results using the exposure measure in Equation (9). The results of estimating

Equation (8) are presented in Table B.13. Panel A shows that the adverse impact of the reform primarily

falls on private firms with a greater baseline reliance on indirect exporting, whereas SOEs are much

better shielded in terms of the reductions in indirect exports and appear to be able to better switch

to direct exporting (however, the estimates are noisy in Column 2). On the other hand, we do not see

much heterogeneity in terms of baseline firm size (Panel B).

So far, the analysis builds on the assumption that we can infer a firm’s indirect exports by comparing

the reported total export revenue in the NBS survey data and the direct exports captured in the Customs

data. However, to the extent that firms may not consider all of their indirect exports as “exports”,

some of the “non-exporters” in the NBS data could well be exporting through FTCs and thus would be

exposed to the reform as well. To examine this possibility, we perform an alternative empirical analysis

that explores heterogeneity across industries in terms of export intensity. We measure export intensity

by the fraction of directly exporting firms in a given 2-digit HS industry (see Table 1 Panel C). The

idea is that if a firm is a “non-exporter” in one of the export-intensive industries (i.e., industries with